中国

中国

India

India

Việt nam

Việt nam

Australia

Australia

대한민국

대한민국

پاکستان

پاکستان

ประเทศไทย

ประเทศไทย

Filipino

Filipino

Malaysia

Malaysia

Bangladesh

Bangladesh

Sri Lanka

Sri Lanka

Indonesia

Indonesia

Узбекистан

Узбекистан

Ireland

Ireland

Česká republika

Česká republika

Türkiye

Türkiye

United Kingdom

United Kingdom

France

France

Deutschland

Deutschland

Nederland

Nederland

España

España

Sverige

Sverige

Italia

Italia

Polska

Polska

Україна

Україна

Português

Português

България

България

Magyarország

Magyarország

Lietuva

Lietuva

Ελλάδα

Ελλάδα

Suomen tasavalta

Suomen tasavalta

United States

United States

Canada

Canada

México

México

Brasil

Brasil

República de Chile

República de Chile

South Africa

South Africa

المملكة العربية السعودية

المملكة العربية السعودية

الجمهورية اللبنانية

الجمهورية اللبنانية

امارات عربية متحدة

امارات عربية متحدة

اليمن

اليمن

المملكة الأردنّيّة الهاشميّة

المملكة الأردنّيّة الهاشميّة

جمهورية مصر العربية

جمهورية مصر العربية

la République Tunisienne

la République Tunisienne

Kenya

Kenya

Tanzania

Tanzania

Nigeria

Nigeria

Other Countries and Regions

Other Countries and Regions

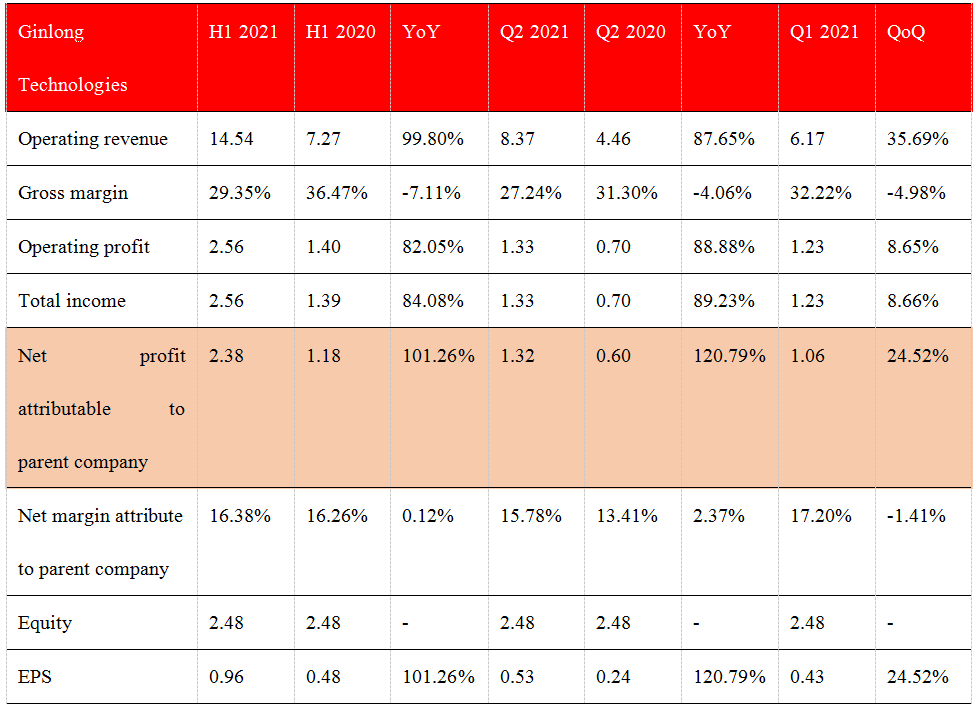

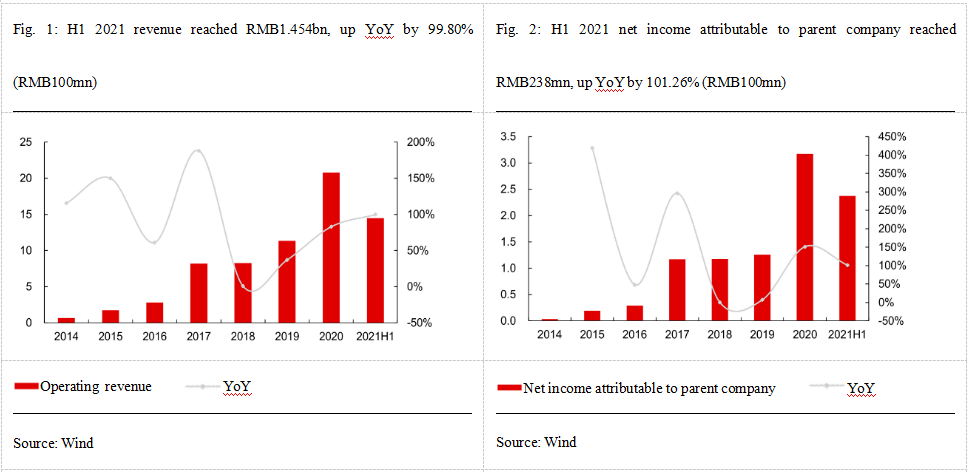

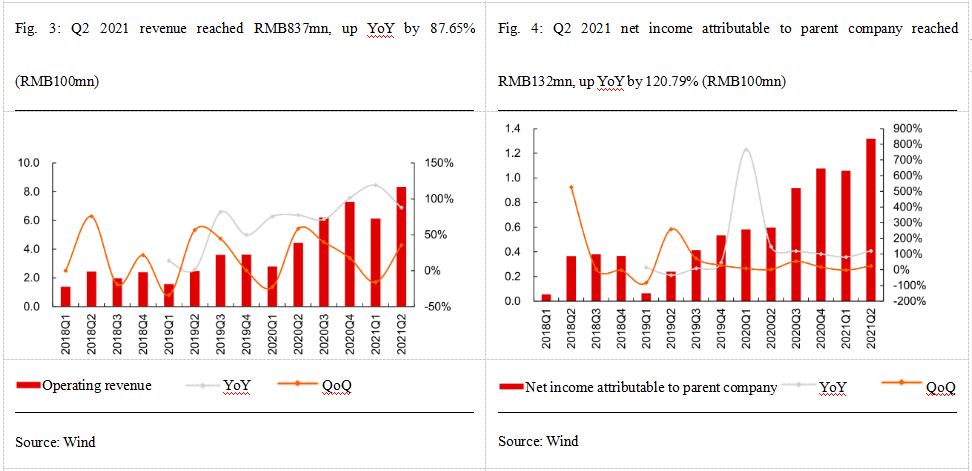

According to the 2021 half year interim report published by Ginlong Technologies, revenue within the reporting period reached RMB1.454bn, up YoY by 99.8%; net income attributable to the parent company reached RMB238mn, up YoY by 101.26%; EPS reached RMB0.96; it is therefore calculated that Q2 revenue was RMB837mn, up YoY by 87.65%, and an increase of 35.69% on the previous quarter; net income attributable to the parent company reached RMB132mn, up YoY by 120.79%; Q2 EPS was RMB0.53, and Q1 EPS was RMB0.43.

Table 1: Summary of Ginlong Technologies’ 2021 Interim Report (RMB100mn)

Source: Wind

Our comments on the interim report are as follows:

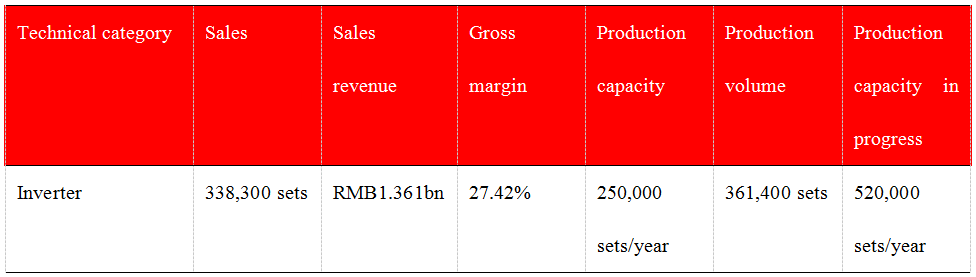

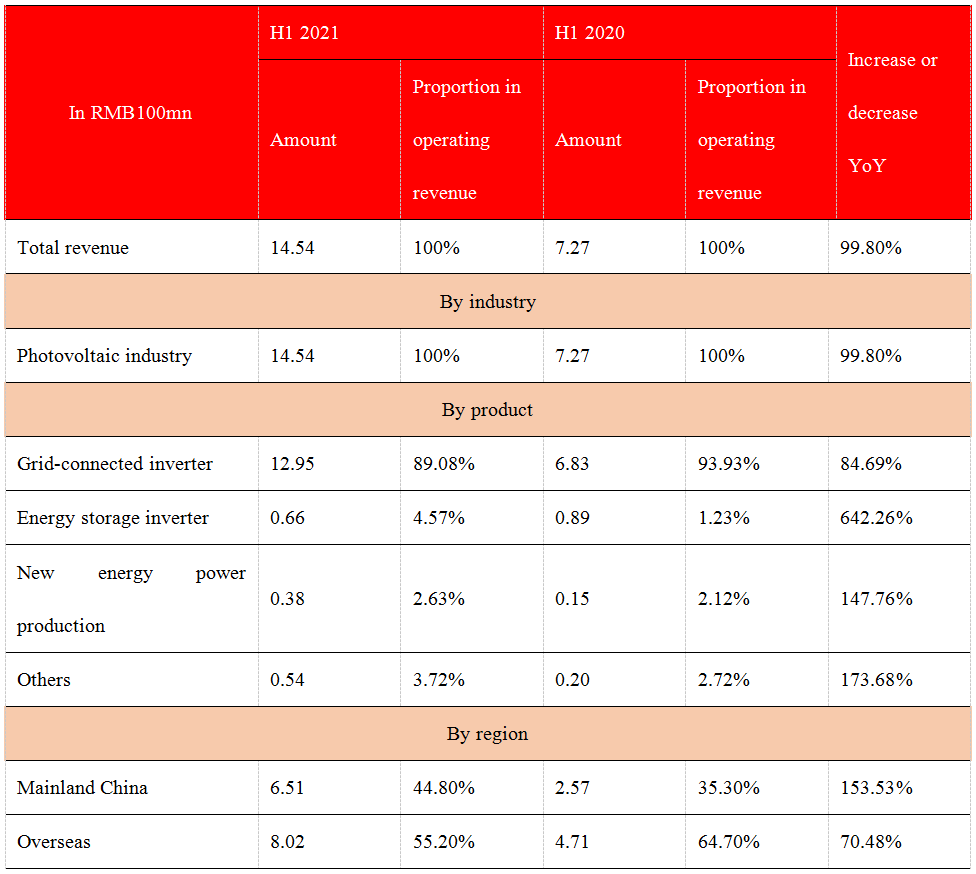

1.The supply and demand sides continue to perform well; production and sale volumes drive doubling of revenue. At the supply side, the inverter industry has faced the problem of chip shortage in 2021. To solve this, the Company signed agreements well in advance to enhance the stock level of IGBT components, and so that the supply of raw materials is guaranteed. At the demand side, domestic residential installed capacity in H1 2021 delivered a remarkable result, reaching 5.86GW, up YoY by 187.42%. Overseas demand was on the rise, especially in India, Germany, Brazil and the US. Inverter export in H1 2021 reached USD 2.145bn, up YoY by 61.38%. Due to the forward thinking and excellent performance of both the supply and demand sides, the Company’s revenue in H1 2021 reached RMB1.454bn, up YoY by 99.80%. The Company produced 361,400 inverters and sold 338,300 of these.

Details by business:

1) Within the grid-connected inverter sector, the Company’s primary business, revenue in H1 2021 reached RMB1.295bn, up YoY by 89.48%;

2) Within the energy storage inverter business, revenue in H1 2021 reached RMB66mn, up YoY by 642.26%.

3) The power station business, the Company has commissioned 151 distributed photovoltaic power stations in H1 2021; installed capacity totaled 140.25MW and revenue from the new energy power production business reached RMB38mn, up YoY by 147.46%.

In H1 2021, the Company continues to increase the development of its overseas market. Revenue from overseas reached RMB802mn, up YoY by 70.48%, and 55.2% of total company revenue, a reduction in share yoy by 9.5%.

Table 2: The Company’s Production and Sale in H1 2021

Source: Wind

Table 3: The Company’s Revenue in H1 2021 (RMB100mn)

Source: Wind

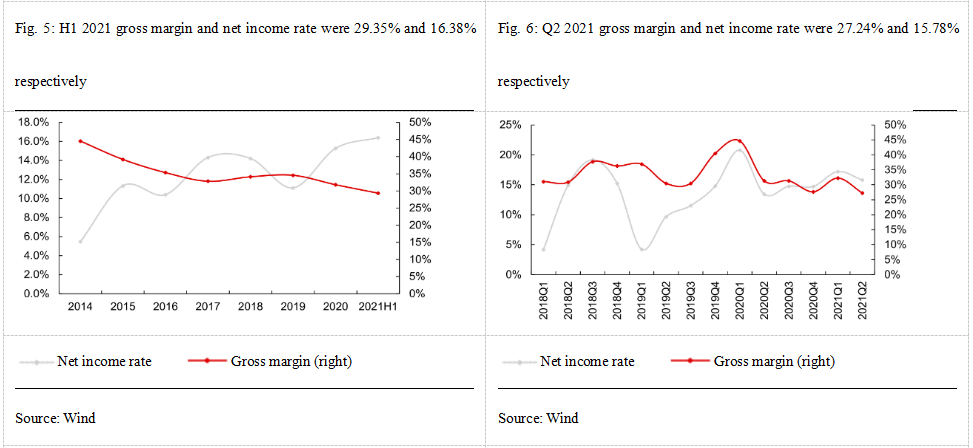

2.Due to rising prices of raw materials and transition of structure to the domestic market, the Company’s profitability declined. In H1 2021, the Company’s comprehensive gross margin was 29.35%, down YoY by 7.11%. The gross margin of the grid-connected inverter business was 26.73%, down YoY by 9.55%.

Details as follows:

1) In response to the rising price of raw materials, the Company transmits the pressure of price downwards to ensure that the gross margin remains within a reasonable range.

2) In the context of increasing domestic demand, the percentage of the Company’s revenue from overseas region in H1 2021 was down to 55.2%. The gross margin of domestic market is normally at least 25% less than that of the overseas market.

3) The inverter sector is relatively independent and less vulnerable to the price competition of the solar modules supply chain, which has meant relatively stable profitability.

Against this background, net income attributable to the parent company in H1 2021 reached RMB238mn, up YoY by 101.26%; net profit not attributable to the parent company reached RMB202mn, up YoY by 69.12%.

3. Despite a decline in Q2 2021 profitability, performance continued to rise. In Q2 2021, revenue reached RMB837mn, up YoY by 87.65%, a result that is mainly attributable to the increase of production and sale volumes. Profitability has remained strong in the face of the rising price of raw materials but Q2 2021 profitability returned to a lower level, and comprehensive gross margin was 27.24%, down YoY by 4.06% and down v’s the previous quarter by 4.98%. Q2 2021 net income attributable to the parent company reached RMB132mn, up YoY by 120.79%.

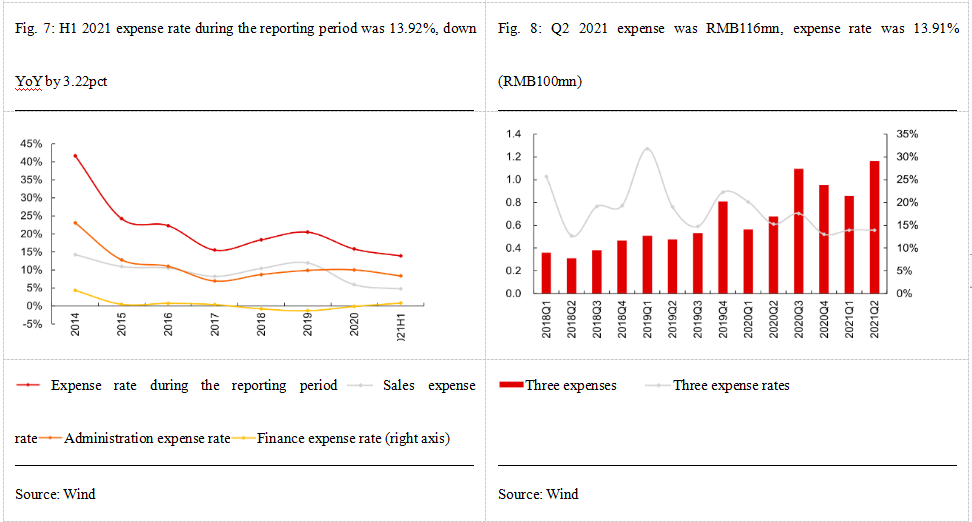

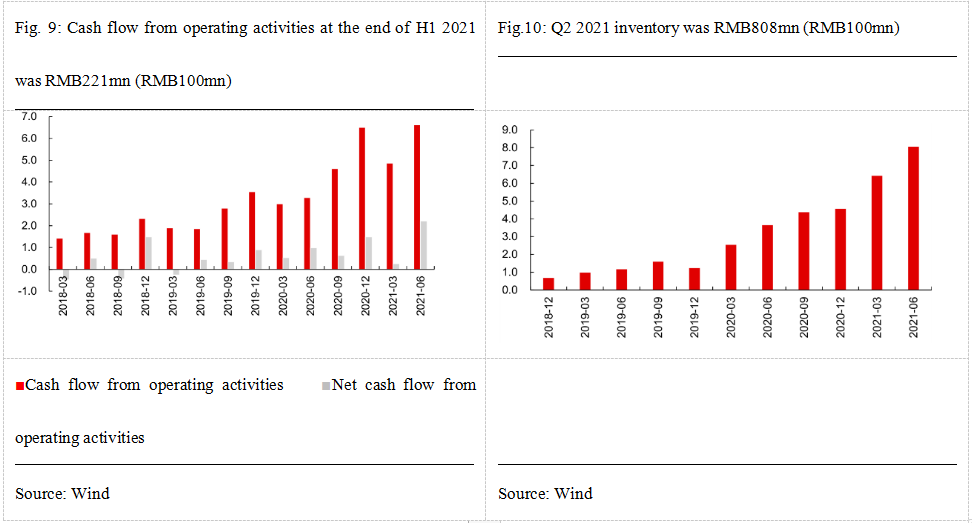

4. R&D expense increased significantly; other business indicators were desirable. In H1 2021, the expense during the reporting period was RMB202mn, and the expense rate was 13.92%, down YoY by 3.22%. The sale expense rate and administration expense rate were 4.75% and 8.36% respectively, and internal affairs were managed and controlled well. The R&D expense rate remained steady, the absolute value of R&D expense increased by RMB32mn to RMB64mn, and the remuneration of R&D personnel increased considerably, which lays the groundwork for product upgrading and replacement. Cash flow at the end of Q2 2021, from operating activities reached RMB221mn, a figure that is far more than RMB99mn as seen in Q2 2020.

5. With acceleration of overseas deployment + increase of user structure + increase of energy storage + stock replacement, the performance was promising.

Regarding the overseas market,The declaration for promoting photovoltaic application projects in entire counties was completed, to which local governments and enterprises actively responded. The planned area and scale is estimated to reach 100GW. As a leading manufacturer of string inverters, the Company launched a promotion system solution for entire counties, and will benefit from the positive tide of photovoltaic applications. With regards to energy storage, the promulgation of new energy storage guidelines and time-of-use power tariff policy not only improves the mechanism, but also stimulates the acceleration of energy storage development. A large-scale market is expected to materialize in the not-too-distant future. The most conservative estimate of domestic energy storage installed capacity is 30GW by 2025. Thanks to the higher premium of energy storage inverter, the Company’s product structure maintains desirable development, and the profit will be increased.

Regarding the overseas market, it is estimated that there is still a space for expansion before 2023. The logic of accelerating inverter exports continues to be viable. If the demand is beyond expectation, the space for expansion will be further increased. At present, the production capacity is 250,000 sets/year, and the new production capacity in progress is 520,000 sets/year. By 2023, the production capacity will rise to 770,000 sets/year, 3 times more than current. Against this background, the Company’s performance in the next two years is promising.

6. To sum up, our estimate is as follows: from 2021 to 2023, the Company’s net income will be RMB615mn, RMB981mn and RMB1.356bn respectively, EPS annually will be RMB0.01, RMB0.01 and RMB0.02 respectively, and PE will be 117X, 73X and 53X respectively. Ginlong Technologies remains as a key recommendation.

Attachment: The financial data is as follows:

2026-06-04 13:44:00.0

2026-04-03 17:18:00.0

Get the latest news of Ginlong at the first time

Asia/Pacific

Europe

North America

South America

Middle East and Africa

Other Countries and Regions